SAPPHIRE BANK

SAPPHIRE BANKCOLORED GEMSTONE INVESTMENT 2026: 8–15% RETURNS & WHERE TO LOOK NOW

The colored gemstone market is entering a new phase. Supply from legacy deposits is tightening. Demand from Asia continues to grow. Auction records are being broken at the top end. Here is what investors need to know about where the market stands — and where it is heading.

THE BIG PICTURE

Colored gemstones outperformed most traditional asset classes over the past decade. Investment-grade sapphires, rubies, and emeralds have appreciated 8–15% annually in the fine and exceptional quality tiers — driven by supply constraints, growing wealth in emerging markets, and a global shift toward tangible assets.

By 2026, the market has matured significantly. Certification is more standardized. Auction transparency has increased. And a new generation of sophisticated collectors treats gemstones as a serious asset class alongside gold, art, and real estate — not a hobby purchase.

This matters for investors: the days of buying uninformed are over. But so are the days of easy arbitrage. Today's market rewards knowledge and patience.

DEMAND DRIVERS IN 2026

China, India, and Southeast Asia now account for an estimated 40–50% of fine colored gemstone demand. As high-net-worth populations in these regions grow, so does appetite for investment-grade stones. Cultural affinity for colored gemstones — particularly rubies in China and sapphires in South Asia — underpins long-term structural demand.

Post-2020, institutional disillusionment with equities and bonds has accelerated interest in hard assets. Gemstones offer a combination that few alternatives can match: genuine scarcity, portability, no counterparty risk, and a track record of holding value through inflation.

The lab-grown diamond market has largely collapsed natural diamond prices at the commercial level. This has redirected high-end jewellery demand toward colored gemstones — which cannot be credibly replicated at scale with the same optical properties. A lab-grown ruby looks different. A Burmese pigeon blood ruby is irreplaceable.

Christie's, Sotheby's, and Phillips continue to set records for top-tier stones. Auction performance creates price anchors and transparency that builds investor confidence — when the highest-quality stones continue to command record prices, it validates the asset class.

SUPPLY: THE STRUCTURAL CONSTRAINT

Supply is the thesis. Unlike gold (continuously mined) or diamonds (whose supply is managed by cartels), fine colored gemstones come from geographically concentrated deposits that are genuinely depleting.

The Padar mines have produced negligible commercial quantities since the 1880s. Every Kashmir sapphire in circulation is antique inventory. Supply is effectively zero — demand is not.

Geopolitical instability and sanctions on Myanmar have constrained supply significantly since 2021. Mogok material still exists, but legal acquisition channels are limited for Western buyers.

The most actively mined premium origin. Production continues, but the finest material (5+ carat unheated royal blue) remains scarce. Sri Lankan government has tightened export controls on rough.

Colombia still produces the world's finest emeralds, but artisanal mining has been under increased regulatory pressure. New large-scale mines have not offset legacy deposit depletion at the top quality tier.

The supply picture is not uniform across quality tiers. Commercial-grade stones remain abundant from secondary origins (Madagascar, Tanzania, Mozambique). The scarcity is concentrated in investment-grade material from prestige origins — which is precisely where returns have been strongest.

2026 MARKET BY CATEGORY

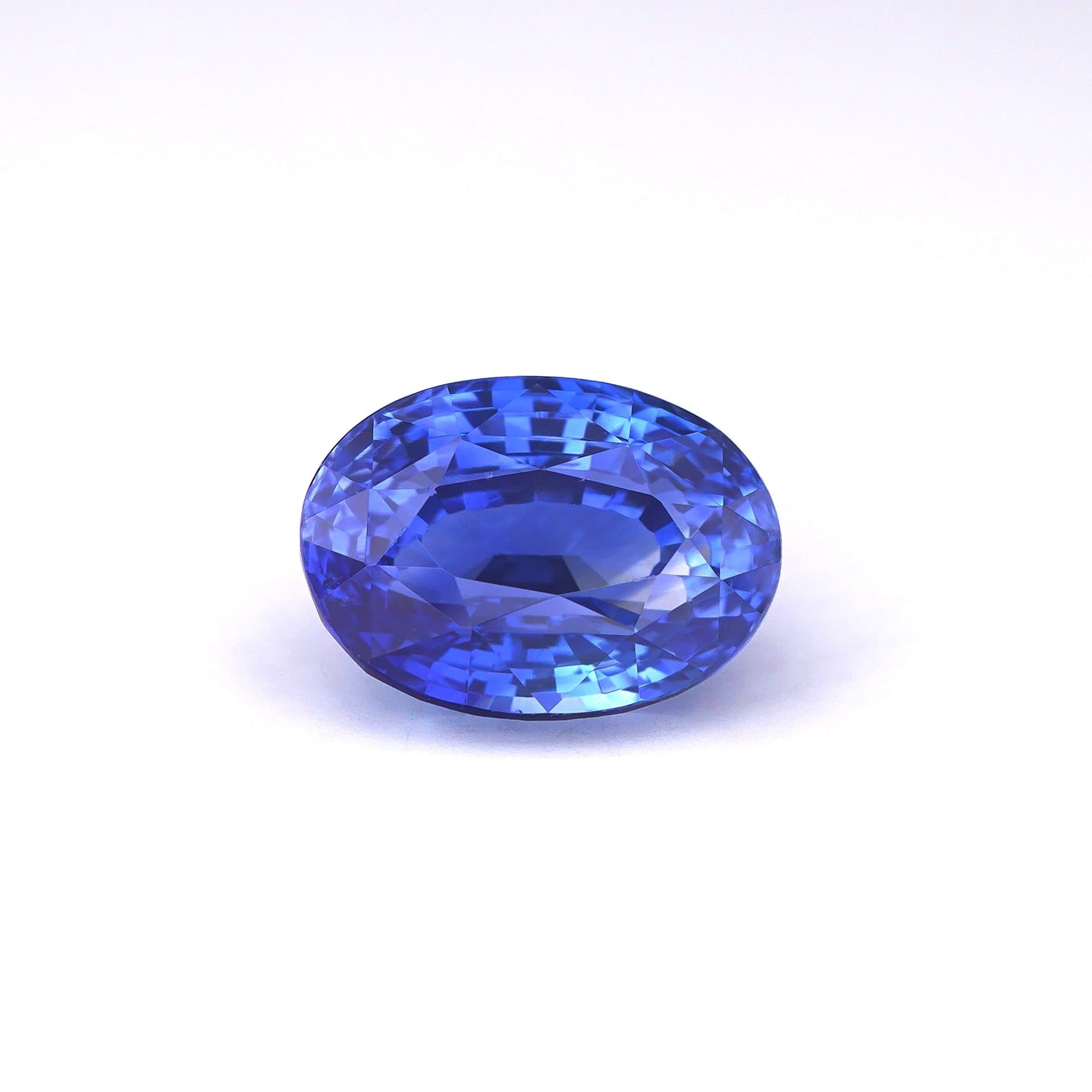

SAPPHIRES

The most liquid colored gemstone market globally. Investment-grade sapphires (2+ carats, unheated, certified origin) have appreciated 8–12% annually over the past five years. Kashmir stones now routinely exceed $80,000/ct at auction for top specimens. Ceylon unheated sapphires in the 3–7 carat range represent the best liquidity-to-appreciation balance for most investors.

RUBIES

Rubies remain the highest price-per-carat colored stone at auction. Burma Mogok with GRS "pigeon blood" designation consistently sets records. However, sanctions complications mean buyers must exercise diligence on provenance. Mozambique rubies offer strong value for investors who want ruby exposure without the geopolitical complexity.

EMERALDS

The most complex investment stone due to ubiquitous treatment (oiling/resin). Untreated or minor-oil Colombian emeralds with Gübelin or GRS certs trade at significant premiums. The clarity grading norms (eye-clean acceptable) require understanding before investing. For most new investors, sapphires or rubies offer a cleaner entry point.

SPINELS

The opportunity category. Spinels are always untreated, genuinely rare, and still underpriced relative to sapphires and rubies of comparable quality. Mahenge neon red and hot pink spinels have appreciated 20%+ annually since 2015. Awareness among Western collectors is growing fast — prices reflect this, but the gap versus sapphires remains wide enough to represent real upside.

CERTIFICATION AS PRICE ANCHOR

One of the most significant structural changes in the market over the past decade is the standardization of top-tier certification. GRS, Gübelin, and SSEF certificates now function as price anchors: the same physical stone can trade at 40–100% different prices with vs without a prestigious lab certificate.

This matters for investors in two ways. First, always buy with a certificate from a recognized lab — it protects resale value and enables auction placement. Second, specific language matters: "no indications of heating," "Burmese origin," or "pigeon blood" designations each carry measurable price premiums that are independently verifiable.

5-YEAR OUTLOOK

The fundamentals for investment-grade colored gemstones remain strong:

- Structural supply deficit at top quality tiers — no new major deposits

- Growing demand from Asia with rising high-net-worth populations

- Lab-grown diamond displacement driving high-end jewellery demand to colored stones

- Continued certification standardization improving market transparency and confidence

- Sanctions complexity around Burma/Myanmar keeping Mogok material constrained

The risks are real: gemstone markets are illiquid compared to equities, exit timing matters, and commercial-grade stones do not share the same supply/demand dynamics as investment-grade material. The maxim holds in 2026 as in any year — buy quality, hold long, sell with documentation.

Projections based on trailing 10-year performance and structural supply/demand analysis. Not financial advice. Past performance does not guarantee future returns.

WHERE TO START IN 2026

For most investors entering the colored gemstone market in 2026, the clearest entry point remains unheated Ceylon sapphires in the 2–5 carat range with GRS or Gübelin certification. They offer:

- The most liquid secondary market of any colored stone category

- Clear certification standards that protect resale value

- Accessible price points vs Kashmir (€15,000–€80,000 range)

- Strong structural appreciation driven by supply constraints

Spinels are the speculative allocation — high upside, lower liquidity, but genuinely undervalued relative to comparable sapphires. Rubies are the premium tier — exceptional returns at the top, but entry prices are high and provenance due diligence is critical.

FREQUENTLY ASKED QUESTIONS

What annual returns have investment-grade colored gemstones produced?

Investment-grade sapphires, rubies, and emeralds have appreciated 8–15% annually over the past decade in the fine and exceptional quality tiers, driven by supply constraints and growing Asian demand.

Which gemstone category offers the best 2025 opportunity?

Spinels are the standout opportunity — genuinely underpriced relative to sapphires and rubies, with Mahenge neon red spinels returning 20%+ annually since 2015. Awareness among Western collectors is growing fast.

Why are colored gemstones benefiting from lab-grown diamonds?

Lab-grown diamonds are available at 80–90% discounts, collapsing natural diamond prices at the commercial level. This is redirecting high-end jewelry demand toward colored gemstones, which cannot be credibly replicated at scale.

What are the projected returns for Kashmir sapphires 2025–2030?

Kashmir sapphires are projected to return 10–15% annually, Burma ruby pigeon blood 10–18%, and Mahenge spinel neon 12–20% — all driven by zero new supply, growing Asian demand, and continued auction record-setting.

RELATED GUIDES

VIEW OUR CURRENT INVENTORY

Every stone we carry is certified, investment-grade, and photographed in detail. Browse our current selection of sapphires, rubies, and spinels.